- Ways to give

- Where to give

- News & impact stories

- Engage Magazine

- Engage: Winter 2025

- Message from the Vice-President, Advancement and Alumni Engagement

- The lasting significance of SFU's opening ceremonies

- Meet Yabome Gilpin-Jackson: Vice-President, People, Equity and Inclusion

- Gibson Art Museum marks new era for arts and culture at SFU

- A place to breathe

- Blueberry research bears fruit at SFU greenhouses

- Your support means the world to us!

- A gift that keeps learning alive for thousands of older adults

- Researching homelessness in suburban communities

- Inspiring the next generation of scientists

- Bridging mathematics and poetry

- SFU's endowment

- Engage: Summer 2025

- Message from the Vice-President, Advancement and Alumni Engagement

- Meet Alison Shaw, Executive Director, SFU Climate Innovation

- Protecting Canada’s aquatic ecosystems

- Red Leafs swim star propelled by donor support

- Creating space for women to thrive in STEM

- Continuing a legacy of artistic innovation

- Going the extra mile: Sue Porter

- Going the extra mile: Kris Nordgren

- Going the extra mile: Barbara Mitchell & Andrew Wister

- How to plan to reduce taxes on your estate: Part three in a three-part series

- Chasing a dream

- Engage: Winter 2024

- Message from the Vice-President, Advancement and Alumni Engagement

- Improving avalanche safety for backcountry adventurers

- Meet Dr. David J. Price

- Archive of beloved CBC show Writers & Company comes to SFU

- Alumnus succeeds courtside with donor support

- More than 42 million thanks!

- Following a different path

- How to plan to reduce taxes on your estate: Part two in a two-part series

- SFU's endowment

- Engage: Summer 2024

- Message from the Vice-President, Advancement and Alumni Engagement

- People of SFU: Meet Annette Santos

- Supporting land-based learning for Indigenous business students

- New award nurtures artists to push creative limits

- Meet the physicians helping lead the journey to B.C.’s new medical school

- Bridging continents for critical international climate research

- Addressing the urgent human health impacts of B.C. wildfires

- Uplifting students in need

- Preserving Vancouver’s community-engaged art history

- Fostering global perspective: A Q&A about paying it forward with alumnus Allan Merrill

- Raising the bar to improve food security for students

- Meet SFU’s 2024 Outstanding Alumni Award recipients

- SFU news and research

- The bold and the Bard

- Inspiring future leaders: a charter alumnus’ legacy

- How to plan to reduce taxes on your estate: Part one in a three-part series

- Gibson Art Museum construction progresses; design earns national recognition

- In Memoriam: Cathy Daminato

- By the numbers

- Engage: Winter 2023

- Message from the Vice-President, Advancement and Alumni Engagement

- People of SFU: Meet Erin Biddlecombe, Senior Director, Student Affairs

- Doing good

- Making dreams come true: One couple's investment in our future

- Five questions to ask when planning a charitable gift in your will

- Healthy food for healthy minds

- Supporting Indigenous and Black scientists

- Part of the bigger picture

- Bridging human connection in the world of immersive technologies

- Bringing equity into the health promotion space

- Transforming the future of cancer

- The singing janitor

- SFU news and research

- Building community and compassion through coffee

- SFU’s endowment: advancing an inclusive and sustainable future

- Message from the Vice-President, Finance and Administration

- Thank you for your impact!

- Engage: Summer 2023

- Message from the Vice-President, Advancement & Alumni Engagement

- People of SFU: Meet Chris (Syeta’xtn) Lewis, Director of Indigenous Initiatives and Reconciliation

- The first graduates of SFU

- By the numbers: investing in the future

- SFU donor community helps student-athlete run through adversity

- Supporting students in hard times

- Through their words: Mathew Fleury

- Through their words: Ashley Kyne

- Through their words: Kali Stierle

- Through their words: Julie Seal

- Strengthening legal services excellence in B.C.

- Coming to SFU: an innovative new hub for the arts

- The power of reciprocity: A Q&A with Ian and Yvonne Reddy

- Transforming Indigenous art education at SFU

- Embracing the SFU student experience

- When charity truly begins at home

- Shaping a more inclusive future in tech

- Propelling diversity and innovation in higher education

- SFU news and research

- Achieving your philanthropic goals with stock options

- In memoriam: Ron Cliff

- Engage: Winter 2025

- Impact of giving

- Engage Magazine

- About us

- Give now

Planning your gift

Your estate plan decisions are unique to your interests and financial situation. Take a moment and look through our many giving options below.

Get in touch to take the next steps

Your estate plans are unique to your interests and financial situation. We're here to answer questions and provide expert guidance at every step.

Rory Green

Director, Gift & Estate Planning

rory_green@sfu.ca

778-782-6799

Gift in will

A gift in your will is a deeply personal, forward-thinking way to give. Once family and friends are cared for, we hope you'll remember SFU. Your legacy will brighten the future of every student who is touched by your generosity.

Additionally, a well-planned gift is ideal when you want to reduce or even eliminate your final income taxes.

Learn more

The most common types of bequests are:

- Residual bequest: SFU receives a portion of the remainder of your estate after other specific gifts have been made.

- Specific bequest: SFU receives a specific dollar amount or stated fraction of your estate or a specified gift of property (collections, art, books, real estate, etc.)

- A percentage (or share) charitable bequest: A gift in a will that designates a specific portion of an estate—such as 5%, 10%, half, or more—to be given to a charity. Unlike a fixed dollar amount, this type of bequest adjusts with the size of the estate, offering flexibility and helping ensure that both loved ones and charitable causes receive a fair share.

- Contingent bequest: SFU would receive a stated share of your estate, but only in the event of the prior death of other named beneficiaries.

- Trust remainder bequest: Named beneficiaries receive income from a trust established in the will. Upon death of the surviving beneficiaries, or at the end of the specified term, all or part of the remaining principal will pass to SFU.

Whether you're considering a major revision of your current will or you're about to have a will drafted for the first time, making a bequest to SFU is easy to do. We're here to answer your questions and provide expert guidance at every step.

Have you already included SFU in your estate plans? Your commitment is sincerely valued, and we want to make sure our information regarding your estate plans is up-to-date and your preferences for recognition are honoured.

Life insurance

Life insurance can be an economical way to create a large and lasting charitable gift, and some policy donations can also result in significant tax savings during your lifetime or for your estate.

We strongly recommend that you fully discuss your options and/or intentions with a professional expert to get advice that's correct for you.

Learn more

Four options, four benefits

- Name SFU as a beneficiary of your insurance policy: Your estate will receive a donation receipt for the value of the policy, which will offset income taxes due to your estate.

- Donate a paid-up policy designating SFU as the irrevocable owner and beneficiary: This will trigger a tax receipt from SFU for the cash surrender value at the time it is transferred.

- Purchase a policy designating SFU as owner and beneficiary: All premium payments can then be claimed as a charitable donation on your tax return.

- Donate ownership of an existing policy and name SFU as a beneficiary: SFU will give a tax receipt for the cash surrender value of the policy, and annual donation receipts will be generated for the value of your premium payments.

Some gifts involving life insurance require pre-approval by the university and others do not. Please connect with us for more information.

RRSPS, RRIFS & TFSAS

Next to personal real estate, registered retirement funds are the most important investment for Canadians. They can be a source of income during our retirement years but can also contribute to our final tax bill, as any remaining value in the fund is fully taxable as income when we pass away.

Using your registered retirement funds to support a gift to SFU can reduce the taxes you pay both now and later.

Learn more

Three options, three benefits:

- Name charitable organizations like SFU as final beneficiaries of your RRSP, RRIF or TFSA: this can eliminate deferred taxes on your funds completely, and leave more money for your loved ones by keeping these assets out of probate.

- Note: If you choose to name SFU as a direct beneficiary, contact your RRSP/RRIF/TFSA sponsor (your bank, investment trust, or insurance company) to determine if a change of beneficiary form needs to be completed.

- Withdraw extra funds from an RRIF or capital from an RRSP or TFSA and donate the same amount: You'll receive a tax receipt offsetting the income tax payable on the withdrawal.

- Use the RRIF withdrawal to pay a premium on a charitable life insurance policy that will leverage your payments for a significant future gift to SFU: Name SFU as the owner and beneficiary of the life insurance policy, and you'll receive a tax receipt offsetting the taxes due on your RRIF withdrawals.

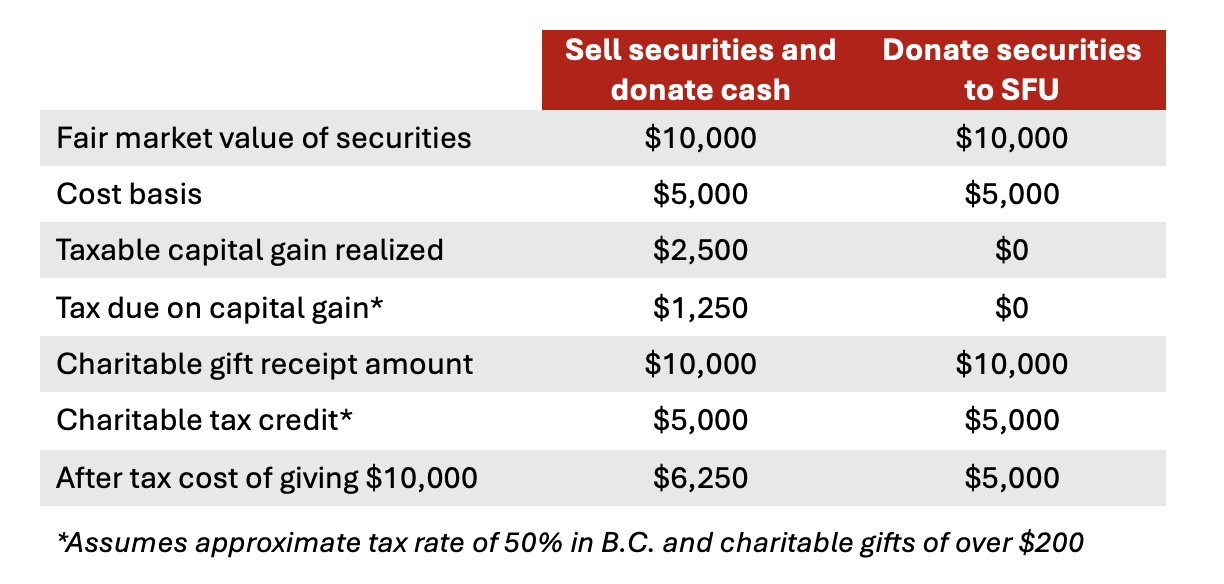

Securities

Donating appreciated securities is simple, cost-effective and the most tax-efficient way to make a charitable gift.

You can make a charitable gift of securities by using any one of the following types: prescribed bonds, units of mutual funds, exchange traded funds (ETFs), shares, warrants and futures that are listed on the stock exchanges prescribed by Canada Revenue Agency.

Learn more

Benefits to you:

- Capital gains income on securities that have been donated to charity are non-taxable - the entire donation amount results in a tax credit.

- Straightforward and easy to transfer: your broker can usually execute a transfer in one or two days.

- Your charitable tax receipt is equal to the mid-point trading value or closing value of your securities, whichever is higher, on the date the securities are received by SFU.

- The proceeds from your securities are directed to the area of your interest.

You can deduct the entire gift in the current year or carry taxes credits forward for up to five years.

*assumes approximate tax rate of 50% in B.C. and charitable gifts over $200.

Interested in gifting securities? Visit our Securities & Stocks page for details.

Stock options

Donations involving employee stock options in a public company can be one of the most tax efficient ways to make a donation.

Learn more

Normally, when stock options are exercised for personal gain, the difference between the stock's fair market value and its exercise price is considered a taxable employment benefit. This benefit is then taxed as a capital gain, such that 50% of the profit is counted as income; employers must withhold the required taxes on that amount, including EI and CPP.

However, charitable gifts arranged by donating stock options can result in a high value gift at low cost.

Benefits to you:

- Reduced cost of giving

- Simple transaction

- Maximized tax benefits

Interested in gifting securities? Visit our Securities & Stocks page for details.

Real estate & personal property

Many Canadians, especially those of us in B.C., have seen tremendous growth in real estate value in recent years. Investment in your primary residence can grow without the tax burden of capital gains, and your primary residence can be passed on to theirs without taxation. However, this is not the case for investment properties and vacation homes.

Learn more

The option to make a gift of real property is a chance to make a significant impact at SFU, as well as avoid paying taxes on gains when selling vacation homes and investment properties.

You can transfer ownership of your property (real estate, works of art, personal collections etc.) as a donation to SFU, and receive a fair market value receipt for tax purposes now or to be used in your estate planning. Additionally, gifts of residual interest may be considered in which you may retain the use of the property during your lifetime.

Benefits to you:

- Immediate tax savings

- Continued use of your property for your lifetime

- Satisfaction of knowing SFU will benefit from your gift in the future

- Your gift passes to the university outside of the estate process, thus reducing your estate probate taxes